Dell Earnings Review: Fiscal Q2 2025

Dell Technologies (NYSE: DELL) reported fiscal Q2 2025 results on Thursday, August 29, 2024. What happened during the release and earnings call, and what are the key points to focus on?

Dell’s Fiscal Q2 2025 Earnings Release

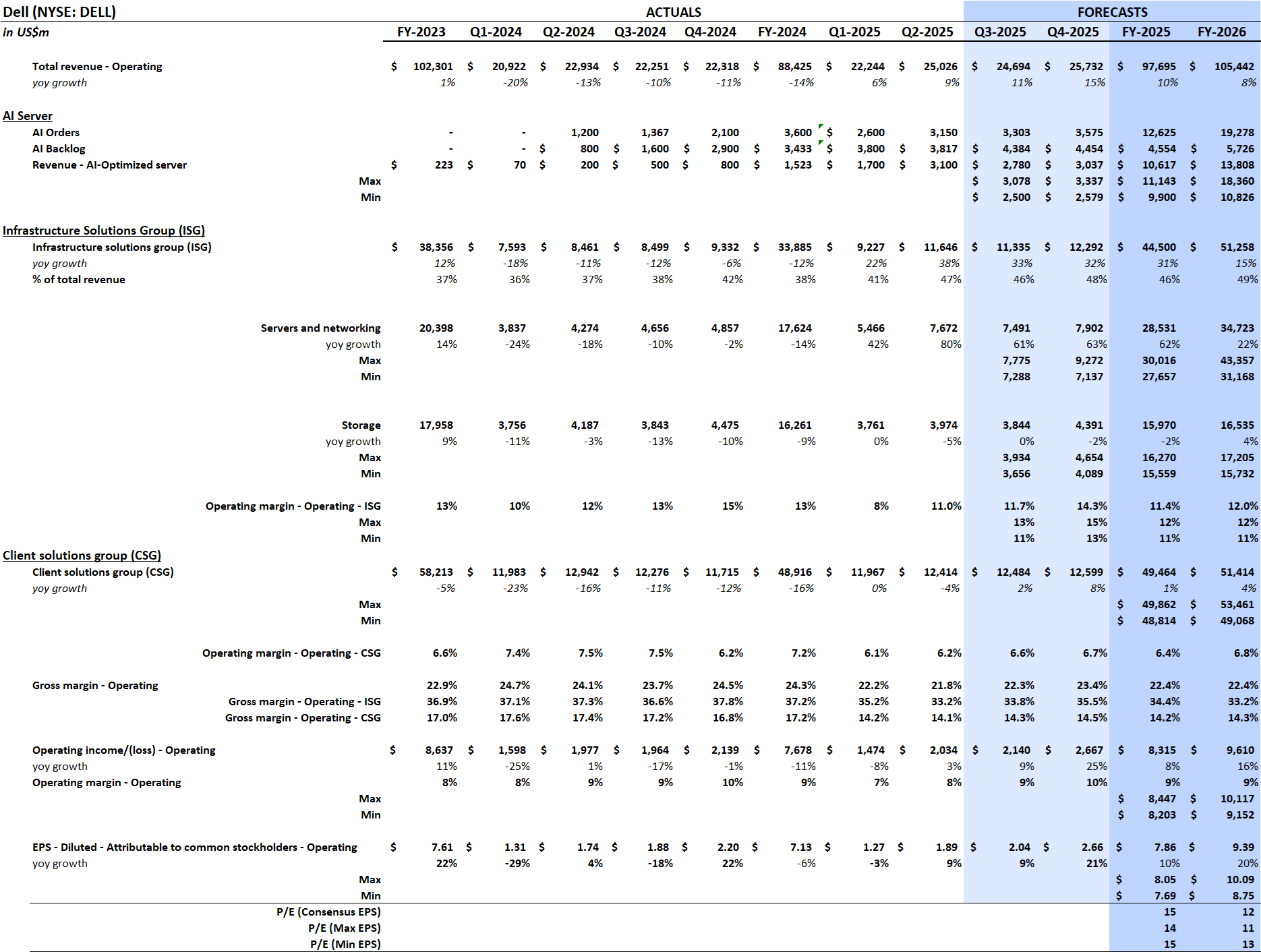

Dell delivered total revenues for Q2 of $25.0 billion, beating Visible Alpha’s consensus estimate of $24.1 billion by $0.9 billion, driven by strong demand for AI servers. The Infrastructure Solutions Group (ISG) segment saw its Q2 revenue surge to $11.6 billion, $1.0 billion ahead of the $10.6 billion consensus estimate coming into the quarter.

The company delivered a respectable AI server backlog of $3.8 billion in Q1, but it led to disappointment in the stock, due to the lack of ISG operating profit growth generated by an additional $1.7 billion in AI server shipments year over year. Dell explained on their earnings call that the headwinds the company saw in Q1 did not persist in Q2. In Q2, the company shipped $3.1 billion of AI servers and the AI server backlog remained at ~$3.8 billion. Training foundational models are still a large percentage of the pipeline. The company is ready to ship more AI servers in Q3, and this is included in the guidance.

The ISG segment’s non-GAAP gross margin came in at 33.2% in Q2, a bit below the consensus of 33.6% and down from 37.3% in Q2 2023. Despite this decline in gross margin, the ISG operating profit margin came in at 11%, ahead of the 10% expected. ISG’s operating profit was expected to generate nearly $1.1 billion in Q2 2024 but, instead, reported $1.3 billion, ahead of last year’s $1.05 billion. In addition, Dell expects the ISG operating margin to continue to improve in the H2.

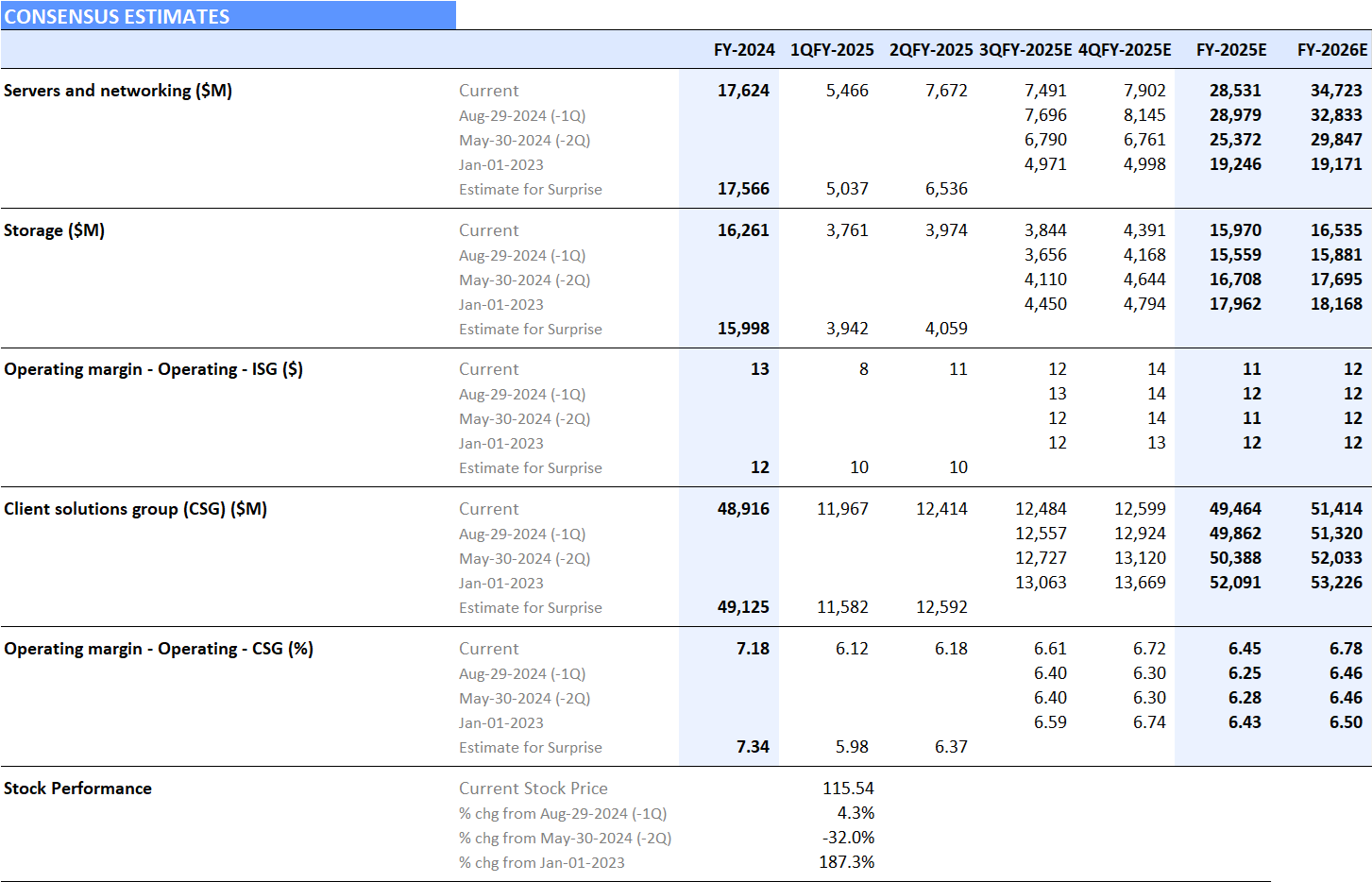

Figure 1: Revisions of Dell estimates

Source: Visible Alpha consensus (September 3, 2024). Stock price data courtesy of FactSet. Dell’s current stock price is as of the market close on August 30, 2024

The Outlook

Near-term growth

For fiscal Q3 2025, Dell guided to $24.0-25.0 billion in total revenue, in line with expectations of $24.7 billion for Q3. The ISG segment revenue is projected to make up $11.3 billion, and to see its margin improve quarter over quarter. The company called out improvements in the storage business and operating expense scaling. The ISG consensus margin for Q3 is expected to be 11.7%, up from 11.0% in Q2.

Long-term outlook

Dell guided FY 2025 revenues to $95.5-98.5 billion, up from $93.5-97.5 billion, in line with the $96.4 billion expected by analysts ahead of Q2. In addition, the company highlighted that ISG will deliver 11-14% long-term margins. Currently, Visible Alpha consensus is projecting ISG’s operating profit margin to jump from 8% in Q1 this fiscal year to over 12% by the end of fiscal year 2026.

Looking further out, analysts remain bullish on the demand for AI servers. Based on six sources, analysts expect to see AI server revenue generate $10.6 billion in FY 2025 and to expand to $13.8 billion in revenue in FY 2026. ISG revenue is expected to grow to $51.3 billion in FY 2026, with nearly all of the year-over-year increase coming from the AI servers. ISG profitability is expected to exceed 11.0% operating profit margin this year and to increase to 12.0% by FY 2026. How long will it take to return to the previous 13% levels?

According to Visible Alpha consensus, EPS is expected to grow nearly 20% from $7.86/share in FY 2025 to $9.39/share in FY 2026. Estimates range from $8.75/share to $10.09/share, putting the FY 2026 P/E consensus at 12x, and in the 11x-13x range.

DELL stock has traded down around 32% since last quarter’s May earnings release, but is up 4% since last week’s most recent announcement on August 29, 2024. Will the ramp in AI servers continue? Will ISG’s profitability return to beat expectations and be a catalyst in H2 2025?

Figure 2: Dell consensus estimates

Source: Visible Alpha consensus (September 3, 2024). Stock price data courtesy of FactSet. Dell’s current stock price is as of the market close on August 30, 2024